Yung and the restless

Yung and the restless

The Deal Magazine

By Ben Fidler

Published July 18, 2008 at 12:42 PM

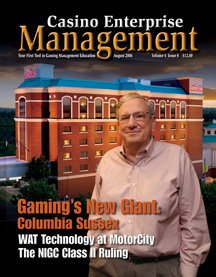

The halcyon days when real estate endlessly rose seems a long way off. But it was only a little more two years ago when Phoenix-based Aztar Corp. found itself to be one of the hottest commodities in Las Vegas. Aztar, the owner of a casino empire stretching from New Jersey to Sin City, owned a 34-acre Tropicana Las Vegas property containing some of the last undeveloped real estate along the Strip. Rivals drooled at the prospects.

So when Aztar put itself up for sale, some gaming notables -- Pinnacle Entertainment Inc., Ameristar Casinos Inc., Colony Capital LLC -- joined the auction. Pinnacle and Ameristar had been duking it out as favorites to win Aztar, but Crestview Hills, Ky.-based Columbia Sussex Corp. emerged as a wild-card bidder and eventually won in May 2006. Columbia Sussex was a hotel company. With Aztar's Vegas property came New Jersey's largest casino, the Tropicana Casino & Resort in Atlantic City, N.J. Columbia Sussex president and CEO William J. Yung III hailed the $2.75 billion acquisition as a "breakthrough transaction" that would create "one of the leading owners, developers and operators of hotels, resorts and casinos."

Yung had reason to gloat. He had waged a brilliant bidding battle for Aztar and won. "That guy wanted to win it at all costs," says one source present at the auction.

Alas, that victory would represent the top for Yung, and it's been a long way down ever since. Today, Yung is gone, having been ousted from the management and board of Tropicana Entertainment LLC, the subsidiary Columbia Sussex created in the aftermath of the Aztar buyout. Tropicana Entertainment filed for Chapter 11 protection in the U.S. Bankruptcy Court for the District of Delaware in Wilmington on May 5. And now the fate of both Tropicana Las Vegas and the Tropicana Casino & Resort in Atlantic City is up in the air again, making bondholders more than a little restless. And to make matters worse, the Tropicana Casino & Resort, which is Tropicana Entertainment's largest source of cash, is now under the supervision of the New Jersey Casino Control Commission and may never be within bondholders' reach.

"This is all uncharted territory," says Scott Butera, a gaming industry veteran who is now running Tropicana Entertainment and sits on its board.

The rise and fall of Yung is a cautionary tale -- one that begins with a dramatic and expensive acquisition, runs through massive management miscues and ends in bankruptcy. In the end, it's the story of a man drawn out of his element by the glitter and flash of a very different business who then makes a series of fatal errors, made worse by an economic cycle that removed any margin for error.

By the time Columbia Sussex purchased Aztar, the company owned 70 hotels, which Yung had assembled through acquisitions in the '70s and '80s. Yung carved out a management style that could be successful in a certain kind of hotel: extracting significant cost savings, typically through extreme job reductions, says one source, who notes, "He cuts the work force down to the bone." Under Yung, staffers were typically required to work longer hours for less money. "That's how he distinguished himself in the hotel business," says the source.

Attempts to contact Yung were unsuccessful, but Butera defends his predecessor. "He built that company from nothing to a company with over 70 hotels," Butera says. "He is a very successful businessman. I've spent a lot of time with him, and I know him to be a man of strong character."

Yung began to dabble in gaming with the 1990 creation of Wimar Tahoe Corp., a vehicle to purchase and run casinos. Among Wimar's stable of assets are the Lake Tahoe Horizon Casino and Resort, the River Palms Hotel and Casino in Laughlin, Nev., the Belle of Baton Rouge, La., and the Lighthouse Point Casino. Although those properties certainly got Yung's feet wet in the gambling business, none of them qualified as a flagship.

Aztar was just what Yung was looking for. It not only had bulk -- 14 casinos in the U.S. and the Caribbean -- but two of its properties were legitimate trophies: the Tropicana Las Vegas and the Tropicana Casino & Resort in Atlantic City.

And, of course, there were those undeveloped acres of land along the Strip. More than two-thirds of the Tropicana Las Vegas' 34-acre footprint was untouched. "The idea was to get a prime piece of property at a time when real estate prices in Vegas were at an all-time high," says Barbara Cappaert, a senior vice president and high-yield bond analyst at KDP Asset Management Co., who's followed gaming for years.

A feeding frenzy ensued. Pinnacle, which at the time owned casinos in Mississippi, Louisiana, Indiana and Argentina, was based in Las Vegas but lacked a casino there, Cappaert says. It, too, needed a flagship, and Tropicana Las Vegas would fit the bill.

The undeveloped acreage held another lure. The source at the Aztar auction explains that Pinnacle wanted to build instead of buy. So the Las Vegas property would kill two birds with one stone. "That was the perfect asset purchase for Pinnacle," the source says. "It's a fit they will probably never see again."

Pinnacle didn't waste time, striking a $2.1 billion deal for Aztar on March 13, 2006. Priced at $38 per share in cash and including $723 million in assumed debt, the deal would kickstart a bidding war. Ameristar on April 3, 2006, supplanted Pinnacle as the leading suitor, offering $42 per share.

Two weeks later, Columbia Sussex showed up, making a $47 per share bid through Wimar Tahoe that shocked participants and analysts. "Columbia Sussex was a bolt out of the blue. Nobody expected them," says the auction source. "They were an unknown quantity. [Nobody knew] how much leverage they had, since they weren't public."

But as Pinnacle, Ameristar, and Colony (which, the source indicates, never made an official bid) discovered, Columbia Sussex wasn't bluffing. Aztar's price had climbed higher and higher and soon eclipsed $50 per share; Ameristar then folded. Pinnacle and Columbia Sussex stared each other down, then Pinnacle folded after Yung offered $54 per share.

Yung found himself deeply into something very different from hotels. For one thing, gaming is highly regulated: Each operator must apply for and receive a gaming license from state authorities. At least one analyst, Brian McGill of Susquehanna Financial Group LLLP, had said that in the heat of the battle for Aztar there was "some concern" over whether Columbia Sussex could get licensed in New Jersey. "In gaming properties, you have to have integrity, you have to have good management and you have to run a first-class operation," says the lawyer for Tropicana Entertainment's bondholders, Ed Weisfelner of law firm Brown Rudnick LLP.

By the middle of 2007, the gaming industry was flagging. Casinos in Atlantic City had already been struggling because of a smoking ban and the emergence of gaming facilities in Pennsylvania.

But Yung pressed forward. To complete his acquisition of the Tropicana AC, he had to go through a procedure called "interim casino authorization," says NJCCC spokesman Daniel Heneghan. "It allows you to go ahead with your business deal while preserving the state's integrity."

Specifically, New Jersey's Division of Gaming Enforcement, or DGE, undertook a full investigation of the casino's practices. In the meantime, Tropicana AC put its casino license into a trust (allowing Columbia Sussex to close the Aztar deal in January 2007). Once the investigation concluded, the NJCCC held hearings.

Typically, the process proceeds smoothly. In fact, only once in 29 years of legal gambling in New Jersey has a company's casino license been revoked. That was in 1989, when the owners of the Atlantis Hotel & Casino were stripped of their license because of financial concerns.

Clearly, Yung thought the process would be perfunctory. He was more focused on the sweeping changes needed at Aztar, given the weakening economy and payments coming due on the debt Tropicana Entertainment shouldered to make the deal. He directed his energies at the Tropicana operation in Atlantic City. He did what he always had done: He began cutting rank-and-file workers at the hotel-casino. This was a particularly sensitive issue for Tropicana, since it had already had issues with its labor unions, according to KDP's Cappaert. "Sometimes, when you're new in an operating market, you can make a move ... that can have bigger ramifications because of the history of the market," she says.

But the Atlantic City workers' union, Unite Here Local 54, wasn't interested in making history. "The unions [there] are very strong," Cappaert says.

The union didn't sue Tropicana Entertainment, and it didn't go on strike. It did something much more devastating: It launched a campaign against Tropicana Entertainment's license renewal in New Jersey.

Union members helped compile information from Tropicana customers about the casino's physical condition, leading to a scathing report by the DGE that argued that cutbacks had led to lousy service and a fall in casino revenue. Local 54 also denounced Tropicana publicly, announcing to media outlets that it was opposed to Tropicana's licensing. It even lobbied the New Jersey Legislature for support and pleaded with the NJCCC to be part of the licensing hearings, which began in November. "The involvement of the union was a little out of the ordinary," says one source. "They normally don't get involved in a licensing hearing."

Tropicana AC's dirty laundry -- literally -- was aired, exposing not only problems with its overall cleanliness but also ugly details about how the casino was managed and how it responded to requests from regulators. Among other things, customer reviews cited in the DGE report criticized the casino for roaches, bedbugs, dirty floors and overflowing garbage pails. Tropicana AC has disputed the use of the reviews.

"The impact of the union's activities to kill our business [is] really working," Yung said at a hearing before the NJCCC on Nov. 21. He also claimed layoffs didn't have "anything to do" with the decline in Tropicana's AC business. "They ... ought to be proud of that," he said of the casino's unions.

They were more livid than proud. Yung had laid off about 1,300 employees at the Tropicana AC by October, saving roughly $40 million.

Despite the Yung-bashing over the job cuts, Butera believes they were among the unpopular things he had to do because of the dramatic shift in the casino market, which was making it much more difficult for the company to come through with its debt payments.

The campaign by the unions only gained steam as the hearings progressed, but what irked the NJCCC and DGE the most wasn't that too many security guards got the ax, but that the Tropicana in Atlantic City lacked a functioning independent audit committee for the first six months after Columbia Sussex assumed control -- flouting the state Casino Control Act requiring such a thing -- and that Yung lied to the NJCCC about the extent of the job cuts.

Court papers depicted Yung telling two different versions of his plan to cut staff, one for investors, the other for NJCCC. Upon applying for interim casino authorization in 2006, Yung testified there "might be some layoffs" but that most of them would come through attrition. However, when looking for financing, Yung told investors that there would be between $30 million and $40 million in savings to be had by slashing staff, as well as other expenses.

Even more damaging were revelations from former Tropicana AC president Fred Buro about a conversation he had with Yung. After preparing for yet another round of job cuts, Buro called Yung from his cell phone to say he had just visited with regulators since it was his "duty" to do so.

"Bill, we have to inform the regulators," Buro testified on Nov. 28 he told Yung. "It's our duty, it's our responsibility. It's my duty to protect this asset, to protect you, protect your license, the property's license."

Yung, Buro testified, responded, "I told you not to tell the regulators. Now you go back and make these cuts or I will find someone else that will."

Last August, Buro was fired.

"He was caught in a couple of lies," Weisfelner says of Yung. "And for an agency responsible for ensuring that casinos are owned and controlled by people showing the highest degree of integrity, I think blatant falsehoods really rankled them."

The hearings dragged on through November and December, leading to a Dec. 12 decision that would send Tropicana Entertainment spiraling toward a Chapter 11 filing. The NJCCC didn't mince words in its ruling. Citing a "lack of business ability, a lack of financial responsibility, and a lack of good character, honesty and integrity," as well as a record of regulatory compliance that was "abysmal," the commission stripped the Tropicana AC of its gaming license. The casino was then placed under the control of Gary S. Stein, a former New Jersey State Supreme Court judge, with the mandate to sell the facility. "It reeks of a lot of the complaints the unions lobbied for," Cappaert says of the NJCCC's "extraordinary" decision. "The company probably just assumed there's no way that they'd lose the license."

The timing couldn't have been worse for Tropicana Entertainment. As Cappaert points out, Yung and the company had been "laying the groundwork" to go public. "It's too bad," she says. "I think their intentions were good. The piling on that they're getting as a result of the [lost] license, I think it's a little too much."

But there was blood in the water, and Tropicana Entertainment bondholders started circling. They hired Weisfelner almost immediately to analyze the bond indenture to see whether the license revocation represented a default or, at the very least, a prospective one. The NJCCC's decision had already triggered a default on about $1.3 billion in Tropicana Entertainment senior debt, leading the company to begin damage control and talks with its lenders on how to resolve the situation and gain more breathing room.

The immediate solution for Tropicana Entertainment was to put another casino on the block: the Casino Aztar in Evansville, Ind. (The company had already struck a deal for the Horizon Casino in Vicksburg, Miss.) It also needed to obtain a waiver on its senior debt. Yung told the banks that, by selling the two casinos and the one in Atlantic City, he could generate enough proceeds to retire the debt and position Tropicana Entertainment for long-term growth.

Unfortunately, Yung never took the trouble to discuss the plan with bondholders. "Yung went out of his way to publicize [that] in his view, his problem was isolated with the banks," Weisfelner says.

The banks appeared to be "pretty well covered" in terms of collateral value, he notes, while bondholders were "ignored." Weisfelner adds, "There's a lot of mistrust."

The Tropicana Entertainment bondholders were already peeved at Yung because of the New Jersey situation. They worried that the company's largest producing assets were being put on the block on a forced-sale basis and were scared that the company would try to cheat them out of equity value in the Las Vegas property.

Their anger only intensified as Yung continued to stonewall them. The bonds are a so-called fulcrum security, which means they are the first security in the Tropicana Entertainment capital structure in which there's not enough collateral to pay off holders in full (for example, if first-lien lenders are getting paid in full in cash, but second-lien holders are getting 50 cents on the dollar, the second liens are holding the fulcrum security).

As Weisfelner says, in a situation where the bonds are the fulcrum security, a company will typically organize talks and agree to pay the fees of the bondholders' attorneys while negotiations progress. But Yung never made either gesture.

So the bondholders had to force their way to the negotiating table. How? By filing a lawsuit against Tropicana Entertainment in the Delaware Court of Chancery on Jan. 28. "We became convinced that there was an immediate default under the bond indenture," Weisfelner says.

At first, that assessment appeared far-fetched. Tropicana Entertainment went on the offensive, calling bondholder assertions that a default took place "simply untrue." The company argued that the bondholders had no right to demand immediate payment and that their actions were jeopardizing the sale of the Tropicana AC. What also appeared to undermine the case of the bondholders was the lack of a provision in the bond indenture that addressed a revocation of a gaming licensing.

"As long as you're current with your bondholder payments, and technically there's nothing else in the indenture [describing a default], they can limp along, say it's not fair and it doesn't matter," KDP's Cappaert says.

Undaunted, bondholders based the suit on five grievances, two of which dealt with an alleged technical default of the indenture. Specifically, bondholders argued that by putting the Tropicana AC under Stein's control, the NJCCC had actually triggered a "disposition of assets," because the stock of Tropicana Entertainment's Adamar of New Jersey Inc. subsidiary had been placed under Stein's care as well. Because of that default, the bondholders contended they had the right to accelerate their debt after 60 days from the time they first asserted a default had occurred.

Though Chancery Vice Chancellor John Noble agreed that the indenture contained no provisions alluding to a gaming license, he argued that "it does not necessarily follow that every consequence flowing from the loss ... is immunized from the reach of the indenture's requirements.

"If a collateral consequence of a license nonrenewal or denial triggers a default provision, the issuer will not be protected merely because the initial precipitating cause was the nonrenewal or denial of the gaming license," he wrote.

Noble reasoned that while appointing Stein didn't create a default by itself, one was tripped when assets were handed over to him, constituting an asset disposition under the indenture that is considered a breach of the agreement. "Title was transferred; the casino assets were disposed of; and the remaining elements of an asset disposition have been satisfied in accordance with the words of the indenture," he wrote.

In his Feb. 28 ruling, Noble decided that the bonds weren't in default immediately. But he did subject Tropicana Entertainment to a pending default, or one that could be asserted at the end of a 60-day period that had already half-expired.

The door was thus flung open for the bondholders. As Weis-

felner recalls thinking, "Now Yung's got to focus on us, because the clock is running."

Tropicana Entertainment didn't exactly sprint into action. It appealed its license revocation to the Appellate Division of the New Jersey Superior Court on March 4, which was nearly three months after the NJCCC ruling. Then Yung and Stein tried a maneuver that sources say incensed the commission again. Rather than appeal Noble's decision, Tropicana Entertainment had Stein go back to the NJCCC to try to get it to approve a method of curing the technical default.

Stein asked the NJCCC to "reconvey," or transfer, the title of the Tropicana AC back to the Adamar subsidiary. The transfer would have served to eliminate the disposition of assets and thus cure the default. But it didn't pass the smell test with the commission, which one source says "excoriated" Stein for taking such a position. "Our gaming counsel said this was undoable as a matter of gaming law," Weisfelner says of Tropicana Entertainment's title transfer attempt. "The commission said [to Stein]: 'This is between the bondholders and Yung. You have no business getting involved in it.'"

Weisfelner says Yung further complicated things by firing his legal counsel, Milbank, Tweed, Hadley & McCloy LLP.

Tropicana Entertainment was really left with only one option, which was to file for bankruptcy. That eventuality gave bondholders the leverage they had been seeking. Tropicana's secured debt was originally scheduled to come due on April 20, but bondholders agreed to a forbearance, if only because they felt the company was ill-positioned at the time to file for Chapter 11. "We didn't want [Yung] to file for bankruptcy without dealing with and making sure that the regulators all over the country were on board," Weisfelner says. "The last thing we wanted to see was regulators yanking licenses and shutting down operations."

Kirkland & Ellis LLP was hired to be Tropicana Entertainment's debtor counsel, and the firm got to work on staging the largest bankruptcy filing of the year.

Tropicana Entertainment already had Butera, a seasoned hand at complex gaming bankruptcies, in the corporate suite. He was the CEO and president of Trump Entertainment Resorts Inc. during its messy 2004-2005 Chapter 11 case and effectively revamped Donald Trump's Atlantic City casino empire. He was serving as the chief operating officer of the Cosmopolitan Resort & Casino in Las Vegas when his phone rang in February.

Tropicana Entertainment's investment banker, Lazard, recruited him for the top spot. "They were looking for someone to spearhead the same kind of thing [as what happened with Trump]," Butera says.

Butera was introduced to Yung and took the job, knowing all about the NJCCC's decision and Tropicana Entertainment's hostile relationship with bondholders. But Butera saw a hidden gem. "It was a very big opportunity," he says. "You've got the fundamentals of a very good company."

With Butera in place, the papers ready and a $67 million debtor-in-possession loan available from Silver Point Finance LLC, Tropicana Entertainment made its filing. Not included in it, however, was Tropicana AC, since it was no longer under Tropicana Entertainment's corporate umbrella.

Again, Tropicana Entertainment tried to get out in front of the situation, claiming in first-day motions that a perfect storm of tough financial conditions had victimized the company. Too much debt, a steep drop in consumer spending and declining real estate values all conspired against the company, and then the cruelest slap -- a "very public, political and vociferous campaign" by the unions.

"We obviously got caught in a very bad market," Butera contends. "Yung bought it at the height of the market only to have to operate it in the trough of the market."

With Tropicana Entertainment now in bankruptcy, the bondholders started viewing Yung as a major distraction and wanted him out. Soon after the filing, Weisfelner didn't even try to disguise the bondholders' intention. "If Yung wasn't there," he said, "I think the restructuring would fall into place fairly quickly and without contentiousness."

The bondholders launched their attack by asking the Delaware court to oust Yung in favor of a trustee, alleging he carried out "grossly misguided business decisions" with an "autocratic and contentious managerial style."

Tropicana Entertainment countered with the proposed establishment of a Butera-headed five-member board, with Yung holding a seat that was to be considered a nonofficer position. The matter headed to a three-day trial in the beginning of July but was diffused after the first day of testimony, when Butera, Kirkland and the bondholders came to a settlement under which Yung would be ousted and the other four board members -- Butera, Thomas Benninger, Michael Corrigan and Bradford Smith -- would all stay. The bondholders, in return, dropped their demands for a trustee.

"From all of our perspectives, not having a trustee was very beneficial," Butera says. "The trustee was a wild card, and I think it was important for us not to lose momentum."

An order approving the settlement was entered on July 3, and while Yung still holds all the equity of Tropicana, he will be hard-pressed to retain any piece of the casino conglomerate he amassed. Most of the time, reorganizations end with equity holders getting wiped out unless they either buy into a more senior piece of the debtor's capital structure or find a way to get all of the company's debt paid off.

In fact, Yung wouldn't get anything until the bondholders are paid back in full. "As it stands now, bondholders would recover less than par," Cappaert says. Adds Weisfelner: "Frankly, I think he's out of the money big time."

Even though Yung is no longer on the scene, bondholders hardly have a clear path to determining their recovery. Tropicana Entertainment's stable of assets, including the Tropicana AC, twists in the wind. Though Stein allegedly drew offers from several prospective buyers for the hotel-casino -- among them Colony Capital; a group formed between Baltimore developer Cordish Co. and former Tropicana AC executive Dennis Gomes; an investor group led by New York developer Joseph Palladino; and Mohegan Sun -- the state of the market and the lack of leverage on Stein's behalf led to bids that he determined were unsatisfactory.

Says Weisfelner, "It's in everyone's interest to buy more time for regulators to see those sales get done in a meaningful way, without having to hit the bid on the low-ball bids we've gotten."

The NJCCC has given Stein more than one extension to sell the Atlantic City casino (his original engagement required a sale within 120 days), but bondholders have moved for a different, and perhaps unprecedented, tack. They have asked the bankruptcy court whether they could initiate discussions with the NJCCC and the DGE in an attempt to get the Atlantic City casino returned to the now Yung-free Tropicana Entertainment and include it in that bankruptcy case. Just how Tropicana Entertainment would adjust its case with Tropicana AC's involvement is unclear. But the company would have to develop a plan and structure the agencies agreed with.

"With Yung gone, I think all of the legal complications to reconveyance are likewise gone," Weisfelner says.

Then there's Tropicana Las Vegas, still the main prize. It's likely it would take more than a Section 363 sale under the federal Bankruptcy Code to truly unlock the potential, and the value, that resides with that property. "The number of people that can afford to buy it is a lot more limited than when Aztar was on the market," the Aztar auction source says. "It's a beautiful asset, but you need deep pockets and lots of patience."

That won't please Tropicana bondholders, but their only choices may be to wait or unload at bargain prices, with the bigger gamble being the former. But on the strength of the Vegas acreage alone, it may be a bet worth taking.

The Deal Magazine

By Ben Fidler

Published July 18, 2008 at 12:42 PM

The halcyon days when real estate endlessly rose seems a long way off. But it was only a little more two years ago when Phoenix-based Aztar Corp. found itself to be one of the hottest commodities in Las Vegas. Aztar, the owner of a casino empire stretching from New Jersey to Sin City, owned a 34-acre Tropicana Las Vegas property containing some of the last undeveloped real estate along the Strip. Rivals drooled at the prospects.

So when Aztar put itself up for sale, some gaming notables -- Pinnacle Entertainment Inc., Ameristar Casinos Inc., Colony Capital LLC -- joined the auction. Pinnacle and Ameristar had been duking it out as favorites to win Aztar, but Crestview Hills, Ky.-based Columbia Sussex Corp. emerged as a wild-card bidder and eventually won in May 2006. Columbia Sussex was a hotel company. With Aztar's Vegas property came New Jersey's largest casino, the Tropicana Casino & Resort in Atlantic City, N.J. Columbia Sussex president and CEO William J. Yung III hailed the $2.75 billion acquisition as a "breakthrough transaction" that would create "one of the leading owners, developers and operators of hotels, resorts and casinos."

Yung had reason to gloat. He had waged a brilliant bidding battle for Aztar and won. "That guy wanted to win it at all costs," says one source present at the auction.

Alas, that victory would represent the top for Yung, and it's been a long way down ever since. Today, Yung is gone, having been ousted from the management and board of Tropicana Entertainment LLC, the subsidiary Columbia Sussex created in the aftermath of the Aztar buyout. Tropicana Entertainment filed for Chapter 11 protection in the U.S. Bankruptcy Court for the District of Delaware in Wilmington on May 5. And now the fate of both Tropicana Las Vegas and the Tropicana Casino & Resort in Atlantic City is up in the air again, making bondholders more than a little restless. And to make matters worse, the Tropicana Casino & Resort, which is Tropicana Entertainment's largest source of cash, is now under the supervision of the New Jersey Casino Control Commission and may never be within bondholders' reach.

"This is all uncharted territory," says Scott Butera, a gaming industry veteran who is now running Tropicana Entertainment and sits on its board.

The rise and fall of Yung is a cautionary tale -- one that begins with a dramatic and expensive acquisition, runs through massive management miscues and ends in bankruptcy. In the end, it's the story of a man drawn out of his element by the glitter and flash of a very different business who then makes a series of fatal errors, made worse by an economic cycle that removed any margin for error.

By the time Columbia Sussex purchased Aztar, the company owned 70 hotels, which Yung had assembled through acquisitions in the '70s and '80s. Yung carved out a management style that could be successful in a certain kind of hotel: extracting significant cost savings, typically through extreme job reductions, says one source, who notes, "He cuts the work force down to the bone." Under Yung, staffers were typically required to work longer hours for less money. "That's how he distinguished himself in the hotel business," says the source.

Attempts to contact Yung were unsuccessful, but Butera defends his predecessor. "He built that company from nothing to a company with over 70 hotels," Butera says. "He is a very successful businessman. I've spent a lot of time with him, and I know him to be a man of strong character."

Yung began to dabble in gaming with the 1990 creation of Wimar Tahoe Corp., a vehicle to purchase and run casinos. Among Wimar's stable of assets are the Lake Tahoe Horizon Casino and Resort, the River Palms Hotel and Casino in Laughlin, Nev., the Belle of Baton Rouge, La., and the Lighthouse Point Casino. Although those properties certainly got Yung's feet wet in the gambling business, none of them qualified as a flagship.

Aztar was just what Yung was looking for. It not only had bulk -- 14 casinos in the U.S. and the Caribbean -- but two of its properties were legitimate trophies: the Tropicana Las Vegas and the Tropicana Casino & Resort in Atlantic City.

And, of course, there were those undeveloped acres of land along the Strip. More than two-thirds of the Tropicana Las Vegas' 34-acre footprint was untouched. "The idea was to get a prime piece of property at a time when real estate prices in Vegas were at an all-time high," says Barbara Cappaert, a senior vice president and high-yield bond analyst at KDP Asset Management Co., who's followed gaming for years.

A feeding frenzy ensued. Pinnacle, which at the time owned casinos in Mississippi, Louisiana, Indiana and Argentina, was based in Las Vegas but lacked a casino there, Cappaert says. It, too, needed a flagship, and Tropicana Las Vegas would fit the bill.

The undeveloped acreage held another lure. The source at the Aztar auction explains that Pinnacle wanted to build instead of buy. So the Las Vegas property would kill two birds with one stone. "That was the perfect asset purchase for Pinnacle," the source says. "It's a fit they will probably never see again."

Pinnacle didn't waste time, striking a $2.1 billion deal for Aztar on March 13, 2006. Priced at $38 per share in cash and including $723 million in assumed debt, the deal would kickstart a bidding war. Ameristar on April 3, 2006, supplanted Pinnacle as the leading suitor, offering $42 per share.

Two weeks later, Columbia Sussex showed up, making a $47 per share bid through Wimar Tahoe that shocked participants and analysts. "Columbia Sussex was a bolt out of the blue. Nobody expected them," says the auction source. "They were an unknown quantity. [Nobody knew] how much leverage they had, since they weren't public."

But as Pinnacle, Ameristar, and Colony (which, the source indicates, never made an official bid) discovered, Columbia Sussex wasn't bluffing. Aztar's price had climbed higher and higher and soon eclipsed $50 per share; Ameristar then folded. Pinnacle and Columbia Sussex stared each other down, then Pinnacle folded after Yung offered $54 per share.

Yung found himself deeply into something very different from hotels. For one thing, gaming is highly regulated: Each operator must apply for and receive a gaming license from state authorities. At least one analyst, Brian McGill of Susquehanna Financial Group LLLP, had said that in the heat of the battle for Aztar there was "some concern" over whether Columbia Sussex could get licensed in New Jersey. "In gaming properties, you have to have integrity, you have to have good management and you have to run a first-class operation," says the lawyer for Tropicana Entertainment's bondholders, Ed Weisfelner of law firm Brown Rudnick LLP.

By the middle of 2007, the gaming industry was flagging. Casinos in Atlantic City had already been struggling because of a smoking ban and the emergence of gaming facilities in Pennsylvania.

But Yung pressed forward. To complete his acquisition of the Tropicana AC, he had to go through a procedure called "interim casino authorization," says NJCCC spokesman Daniel Heneghan. "It allows you to go ahead with your business deal while preserving the state's integrity."

Specifically, New Jersey's Division of Gaming Enforcement, or DGE, undertook a full investigation of the casino's practices. In the meantime, Tropicana AC put its casino license into a trust (allowing Columbia Sussex to close the Aztar deal in January 2007). Once the investigation concluded, the NJCCC held hearings.

Typically, the process proceeds smoothly. In fact, only once in 29 years of legal gambling in New Jersey has a company's casino license been revoked. That was in 1989, when the owners of the Atlantis Hotel & Casino were stripped of their license because of financial concerns.

Clearly, Yung thought the process would be perfunctory. He was more focused on the sweeping changes needed at Aztar, given the weakening economy and payments coming due on the debt Tropicana Entertainment shouldered to make the deal. He directed his energies at the Tropicana operation in Atlantic City. He did what he always had done: He began cutting rank-and-file workers at the hotel-casino. This was a particularly sensitive issue for Tropicana, since it had already had issues with its labor unions, according to KDP's Cappaert. "Sometimes, when you're new in an operating market, you can make a move ... that can have bigger ramifications because of the history of the market," she says.

But the Atlantic City workers' union, Unite Here Local 54, wasn't interested in making history. "The unions [there] are very strong," Cappaert says.

The union didn't sue Tropicana Entertainment, and it didn't go on strike. It did something much more devastating: It launched a campaign against Tropicana Entertainment's license renewal in New Jersey.

Union members helped compile information from Tropicana customers about the casino's physical condition, leading to a scathing report by the DGE that argued that cutbacks had led to lousy service and a fall in casino revenue. Local 54 also denounced Tropicana publicly, announcing to media outlets that it was opposed to Tropicana's licensing. It even lobbied the New Jersey Legislature for support and pleaded with the NJCCC to be part of the licensing hearings, which began in November. "The involvement of the union was a little out of the ordinary," says one source. "They normally don't get involved in a licensing hearing."

Tropicana AC's dirty laundry -- literally -- was aired, exposing not only problems with its overall cleanliness but also ugly details about how the casino was managed and how it responded to requests from regulators. Among other things, customer reviews cited in the DGE report criticized the casino for roaches, bedbugs, dirty floors and overflowing garbage pails. Tropicana AC has disputed the use of the reviews.

"The impact of the union's activities to kill our business [is] really working," Yung said at a hearing before the NJCCC on Nov. 21. He also claimed layoffs didn't have "anything to do" with the decline in Tropicana's AC business. "They ... ought to be proud of that," he said of the casino's unions.

They were more livid than proud. Yung had laid off about 1,300 employees at the Tropicana AC by October, saving roughly $40 million.

Despite the Yung-bashing over the job cuts, Butera believes they were among the unpopular things he had to do because of the dramatic shift in the casino market, which was making it much more difficult for the company to come through with its debt payments.

The campaign by the unions only gained steam as the hearings progressed, but what irked the NJCCC and DGE the most wasn't that too many security guards got the ax, but that the Tropicana in Atlantic City lacked a functioning independent audit committee for the first six months after Columbia Sussex assumed control -- flouting the state Casino Control Act requiring such a thing -- and that Yung lied to the NJCCC about the extent of the job cuts.

Court papers depicted Yung telling two different versions of his plan to cut staff, one for investors, the other for NJCCC. Upon applying for interim casino authorization in 2006, Yung testified there "might be some layoffs" but that most of them would come through attrition. However, when looking for financing, Yung told investors that there would be between $30 million and $40 million in savings to be had by slashing staff, as well as other expenses.

Even more damaging were revelations from former Tropicana AC president Fred Buro about a conversation he had with Yung. After preparing for yet another round of job cuts, Buro called Yung from his cell phone to say he had just visited with regulators since it was his "duty" to do so.

"Bill, we have to inform the regulators," Buro testified on Nov. 28 he told Yung. "It's our duty, it's our responsibility. It's my duty to protect this asset, to protect you, protect your license, the property's license."

Yung, Buro testified, responded, "I told you not to tell the regulators. Now you go back and make these cuts or I will find someone else that will."

Last August, Buro was fired.

"He was caught in a couple of lies," Weisfelner says of Yung. "And for an agency responsible for ensuring that casinos are owned and controlled by people showing the highest degree of integrity, I think blatant falsehoods really rankled them."

The hearings dragged on through November and December, leading to a Dec. 12 decision that would send Tropicana Entertainment spiraling toward a Chapter 11 filing. The NJCCC didn't mince words in its ruling. Citing a "lack of business ability, a lack of financial responsibility, and a lack of good character, honesty and integrity," as well as a record of regulatory compliance that was "abysmal," the commission stripped the Tropicana AC of its gaming license. The casino was then placed under the control of Gary S. Stein, a former New Jersey State Supreme Court judge, with the mandate to sell the facility. "It reeks of a lot of the complaints the unions lobbied for," Cappaert says of the NJCCC's "extraordinary" decision. "The company probably just assumed there's no way that they'd lose the license."

The timing couldn't have been worse for Tropicana Entertainment. As Cappaert points out, Yung and the company had been "laying the groundwork" to go public. "It's too bad," she says. "I think their intentions were good. The piling on that they're getting as a result of the [lost] license, I think it's a little too much."

But there was blood in the water, and Tropicana Entertainment bondholders started circling. They hired Weisfelner almost immediately to analyze the bond indenture to see whether the license revocation represented a default or, at the very least, a prospective one. The NJCCC's decision had already triggered a default on about $1.3 billion in Tropicana Entertainment senior debt, leading the company to begin damage control and talks with its lenders on how to resolve the situation and gain more breathing room.

The immediate solution for Tropicana Entertainment was to put another casino on the block: the Casino Aztar in Evansville, Ind. (The company had already struck a deal for the Horizon Casino in Vicksburg, Miss.) It also needed to obtain a waiver on its senior debt. Yung told the banks that, by selling the two casinos and the one in Atlantic City, he could generate enough proceeds to retire the debt and position Tropicana Entertainment for long-term growth.

Unfortunately, Yung never took the trouble to discuss the plan with bondholders. "Yung went out of his way to publicize [that] in his view, his problem was isolated with the banks," Weisfelner says.

The banks appeared to be "pretty well covered" in terms of collateral value, he notes, while bondholders were "ignored." Weisfelner adds, "There's a lot of mistrust."

The Tropicana Entertainment bondholders were already peeved at Yung because of the New Jersey situation. They worried that the company's largest producing assets were being put on the block on a forced-sale basis and were scared that the company would try to cheat them out of equity value in the Las Vegas property.

Their anger only intensified as Yung continued to stonewall them. The bonds are a so-called fulcrum security, which means they are the first security in the Tropicana Entertainment capital structure in which there's not enough collateral to pay off holders in full (for example, if first-lien lenders are getting paid in full in cash, but second-lien holders are getting 50 cents on the dollar, the second liens are holding the fulcrum security).

As Weisfelner says, in a situation where the bonds are the fulcrum security, a company will typically organize talks and agree to pay the fees of the bondholders' attorneys while negotiations progress. But Yung never made either gesture.

So the bondholders had to force their way to the negotiating table. How? By filing a lawsuit against Tropicana Entertainment in the Delaware Court of Chancery on Jan. 28. "We became convinced that there was an immediate default under the bond indenture," Weisfelner says.

At first, that assessment appeared far-fetched. Tropicana Entertainment went on the offensive, calling bondholder assertions that a default took place "simply untrue." The company argued that the bondholders had no right to demand immediate payment and that their actions were jeopardizing the sale of the Tropicana AC. What also appeared to undermine the case of the bondholders was the lack of a provision in the bond indenture that addressed a revocation of a gaming licensing.

"As long as you're current with your bondholder payments, and technically there's nothing else in the indenture [describing a default], they can limp along, say it's not fair and it doesn't matter," KDP's Cappaert says.

Undaunted, bondholders based the suit on five grievances, two of which dealt with an alleged technical default of the indenture. Specifically, bondholders argued that by putting the Tropicana AC under Stein's control, the NJCCC had actually triggered a "disposition of assets," because the stock of Tropicana Entertainment's Adamar of New Jersey Inc. subsidiary had been placed under Stein's care as well. Because of that default, the bondholders contended they had the right to accelerate their debt after 60 days from the time they first asserted a default had occurred.

Though Chancery Vice Chancellor John Noble agreed that the indenture contained no provisions alluding to a gaming license, he argued that "it does not necessarily follow that every consequence flowing from the loss ... is immunized from the reach of the indenture's requirements.

"If a collateral consequence of a license nonrenewal or denial triggers a default provision, the issuer will not be protected merely because the initial precipitating cause was the nonrenewal or denial of the gaming license," he wrote.

Noble reasoned that while appointing Stein didn't create a default by itself, one was tripped when assets were handed over to him, constituting an asset disposition under the indenture that is considered a breach of the agreement. "Title was transferred; the casino assets were disposed of; and the remaining elements of an asset disposition have been satisfied in accordance with the words of the indenture," he wrote.

In his Feb. 28 ruling, Noble decided that the bonds weren't in default immediately. But he did subject Tropicana Entertainment to a pending default, or one that could be asserted at the end of a 60-day period that had already half-expired.

The door was thus flung open for the bondholders. As Weis-

felner recalls thinking, "Now Yung's got to focus on us, because the clock is running."

Tropicana Entertainment didn't exactly sprint into action. It appealed its license revocation to the Appellate Division of the New Jersey Superior Court on March 4, which was nearly three months after the NJCCC ruling. Then Yung and Stein tried a maneuver that sources say incensed the commission again. Rather than appeal Noble's decision, Tropicana Entertainment had Stein go back to the NJCCC to try to get it to approve a method of curing the technical default.

Stein asked the NJCCC to "reconvey," or transfer, the title of the Tropicana AC back to the Adamar subsidiary. The transfer would have served to eliminate the disposition of assets and thus cure the default. But it didn't pass the smell test with the commission, which one source says "excoriated" Stein for taking such a position. "Our gaming counsel said this was undoable as a matter of gaming law," Weisfelner says of Tropicana Entertainment's title transfer attempt. "The commission said [to Stein]: 'This is between the bondholders and Yung. You have no business getting involved in it.'"

Weisfelner says Yung further complicated things by firing his legal counsel, Milbank, Tweed, Hadley & McCloy LLP.

Tropicana Entertainment was really left with only one option, which was to file for bankruptcy. That eventuality gave bondholders the leverage they had been seeking. Tropicana's secured debt was originally scheduled to come due on April 20, but bondholders agreed to a forbearance, if only because they felt the company was ill-positioned at the time to file for Chapter 11. "We didn't want [Yung] to file for bankruptcy without dealing with and making sure that the regulators all over the country were on board," Weisfelner says. "The last thing we wanted to see was regulators yanking licenses and shutting down operations."

Kirkland & Ellis LLP was hired to be Tropicana Entertainment's debtor counsel, and the firm got to work on staging the largest bankruptcy filing of the year.

Tropicana Entertainment already had Butera, a seasoned hand at complex gaming bankruptcies, in the corporate suite. He was the CEO and president of Trump Entertainment Resorts Inc. during its messy 2004-2005 Chapter 11 case and effectively revamped Donald Trump's Atlantic City casino empire. He was serving as the chief operating officer of the Cosmopolitan Resort & Casino in Las Vegas when his phone rang in February.

Tropicana Entertainment's investment banker, Lazard, recruited him for the top spot. "They were looking for someone to spearhead the same kind of thing [as what happened with Trump]," Butera says.

Butera was introduced to Yung and took the job, knowing all about the NJCCC's decision and Tropicana Entertainment's hostile relationship with bondholders. But Butera saw a hidden gem. "It was a very big opportunity," he says. "You've got the fundamentals of a very good company."

With Butera in place, the papers ready and a $67 million debtor-in-possession loan available from Silver Point Finance LLC, Tropicana Entertainment made its filing. Not included in it, however, was Tropicana AC, since it was no longer under Tropicana Entertainment's corporate umbrella.

Again, Tropicana Entertainment tried to get out in front of the situation, claiming in first-day motions that a perfect storm of tough financial conditions had victimized the company. Too much debt, a steep drop in consumer spending and declining real estate values all conspired against the company, and then the cruelest slap -- a "very public, political and vociferous campaign" by the unions.

"We obviously got caught in a very bad market," Butera contends. "Yung bought it at the height of the market only to have to operate it in the trough of the market."

With Tropicana Entertainment now in bankruptcy, the bondholders started viewing Yung as a major distraction and wanted him out. Soon after the filing, Weisfelner didn't even try to disguise the bondholders' intention. "If Yung wasn't there," he said, "I think the restructuring would fall into place fairly quickly and without contentiousness."

The bondholders launched their attack by asking the Delaware court to oust Yung in favor of a trustee, alleging he carried out "grossly misguided business decisions" with an "autocratic and contentious managerial style."

Tropicana Entertainment countered with the proposed establishment of a Butera-headed five-member board, with Yung holding a seat that was to be considered a nonofficer position. The matter headed to a three-day trial in the beginning of July but was diffused after the first day of testimony, when Butera, Kirkland and the bondholders came to a settlement under which Yung would be ousted and the other four board members -- Butera, Thomas Benninger, Michael Corrigan and Bradford Smith -- would all stay. The bondholders, in return, dropped their demands for a trustee.

"From all of our perspectives, not having a trustee was very beneficial," Butera says. "The trustee was a wild card, and I think it was important for us not to lose momentum."

An order approving the settlement was entered on July 3, and while Yung still holds all the equity of Tropicana, he will be hard-pressed to retain any piece of the casino conglomerate he amassed. Most of the time, reorganizations end with equity holders getting wiped out unless they either buy into a more senior piece of the debtor's capital structure or find a way to get all of the company's debt paid off.

In fact, Yung wouldn't get anything until the bondholders are paid back in full. "As it stands now, bondholders would recover less than par," Cappaert says. Adds Weisfelner: "Frankly, I think he's out of the money big time."

Even though Yung is no longer on the scene, bondholders hardly have a clear path to determining their recovery. Tropicana Entertainment's stable of assets, including the Tropicana AC, twists in the wind. Though Stein allegedly drew offers from several prospective buyers for the hotel-casino -- among them Colony Capital; a group formed between Baltimore developer Cordish Co. and former Tropicana AC executive Dennis Gomes; an investor group led by New York developer Joseph Palladino; and Mohegan Sun -- the state of the market and the lack of leverage on Stein's behalf led to bids that he determined were unsatisfactory.

Says Weisfelner, "It's in everyone's interest to buy more time for regulators to see those sales get done in a meaningful way, without having to hit the bid on the low-ball bids we've gotten."

The NJCCC has given Stein more than one extension to sell the Atlantic City casino (his original engagement required a sale within 120 days), but bondholders have moved for a different, and perhaps unprecedented, tack. They have asked the bankruptcy court whether they could initiate discussions with the NJCCC and the DGE in an attempt to get the Atlantic City casino returned to the now Yung-free Tropicana Entertainment and include it in that bankruptcy case. Just how Tropicana Entertainment would adjust its case with Tropicana AC's involvement is unclear. But the company would have to develop a plan and structure the agencies agreed with.

"With Yung gone, I think all of the legal complications to reconveyance are likewise gone," Weisfelner says.

Then there's Tropicana Las Vegas, still the main prize. It's likely it would take more than a Section 363 sale under the federal Bankruptcy Code to truly unlock the potential, and the value, that resides with that property. "The number of people that can afford to buy it is a lot more limited than when Aztar was on the market," the Aztar auction source says. "It's a beautiful asset, but you need deep pockets and lots of patience."

That won't please Tropicana bondholders, but their only choices may be to wait or unload at bargain prices, with the bigger gamble being the former. But on the strength of the Vegas acreage alone, it may be a bet worth taking.

posted by Fred A. Buro at 5:03 AM

0 comments

![]()

{kind=link}